The government recently launched National Pension System Vatsalya (NPS Vatsalya), a retirement saving scheme for children that was introduced in the Union Budget for 2024-25 on July 23.

What is the NPS Vatsalya scheme?

Eligibility for NPS Vatsalya:

Age requirement: Open to all minor citizens (below 18 years).

Account operation: Can be opened in the name of a minor, operated by a parent or guardian. The minor is the beneficiary.

Opening channels: Accounts can be opened through various Points of Presence regulated by PFRDA, including major banks, India Post, Pension Funds, and online platforms (e-NPS).

Minimum contribution: A minimum contribution of Rs 1,000 per annum is required, with no maximum limit on contributions.

Investment choices: PFRDA lets subscribers invest in government securities, corporate debt and equity in different properties, depending on their risk appetite and return expectations.

How can you create a big corpus for your child with the help of NPS Vatsalya?

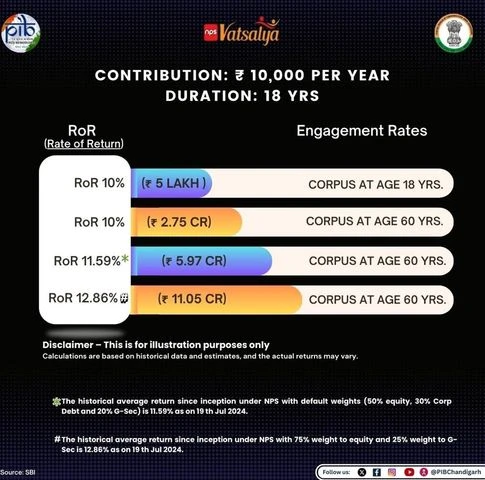

According to a post on X by the Press Information Bureau in Chandigarh, here’s how much your child can save with NPS Vatsalya:

– Annual contribution: Rs 10,000

– Investment duration: 18 years

– Estimated corpus at age 18: Rs 5 lakh (assuming a 10 per cent rate of return)

– Estimated corpus at age 60:

– At a 10 per cent rate of return: Rs 2.75 crore

– At an 11.59 per cent* rate of return: Rs 5.97 crore

– At a 12.86 per cent# rate of return: Rs 11.05 crore

"NPS Vatsalya Scheme: How you can create corpus for your child with the help of NPS Vatsalya | Personal Finance")

“NPS Vatsalya is an excellent tool to help you build a substantial corpus for your child’s future. Start early and contribute regularly, even small amounts can make a big difference over time. Choose a suitable investment option based on your child’s future needs and maximise your contributions,” said Ritika Nayyar, partner, Singhania & Co.

“Monitor and adjust your investments regularly to ensure they align with your child’s risk tolerance and financial goals. NPS Vatsalya is a long-term investment. It’s important to maintain a disciplined approach and stay focused on your child’s future financial security,” she said.

How to open an NPS Vatsalya account

You may open an NPS Vatsalya account offline and online through the eNPS platform.

This online system simplifies the registration process and allows users to easily make additional contributions, making it more efficient and user-friendly.

You can register with any of the Central Recordkeeping Agencies (CRAs) such as Protean, KFintech, or Cams NPS.

You can also open an NPS account in banks. Here are a few banks that have launched the NPS Vatsalya scheme.

Axis Bank: Visit their closest Axis Bank branch with necessary documents such as the child’s birth certificate, PAN card, and card.

ICICI Bank: To register for NPS Vatsalya, customers can visit their nearest ICICI Bank business centre

Canara Bank: Visit your nearest bank branch or visit http://pfrda.org.in

Punjab National Bank: To apply online and for more info, visit: https://pnbindia.in/NPS.html

Central Bank of India: You can open an account through all branches; or use the link: https://www.centralbank.net.in/jsp/NPS.html .

Bank of Maharashtra: You can open account using the link to invest in NPS Vatsalya: https://bankofmaharashtra.in/nps-vatsalya#:~:

Documents needed to open NPS account

Date of birth proof (for the minor):

Birth certificate

School leaving certificate

PAN Card

Passport

KYC documents for the guardian:

Aadhaar Card

Driving Licence

Passport

Voter ID Card

NREGA Job Card

Documents from the National Population Register (NPR)

Bank account:

If the guardian is an NRI:

A Non-Resident External (NRE) or Non-Resident Ordinary (NRO) bank account (either solo or joint) must be opened specifically for the minor.

First Published: Sep 20 2024 | 5:31 PM IST

{kind=link}